Many individuals around the world are familiar with the name, John Pierpont Morgan. J.P. Morgan Chase is one of the largest banks and financial service providers in the world. Despite this level of fame, few people know the story and the significance of the man behind the name.

| Born on April 17, 1837 in Hartford, Connecticut, John Pierpont Morgan grew up in a wealthy family. His grandfather had established the family in Hartford by investing in real estate, steamboat lines, and railroads. His father, Junius Spencer Morgan, continued to expand the family wealth by partnering in a firm which controlled and financed the majority of the Atlantic cotton trade. Through his many business connections, J.S. Morgan , befriended George Peabody, a leading banker in London. J.S. Morgan took over Peabody's bank upon Peabody's retirement in the 1860s (Gordon, 1989). Hence, from a very young age, J.P. Morgan understood the significance and workings of international banking and business. |

This deep understanding J.P. Morgan possessed, paired with his good character, helped create the Wall Street giant that he became. Throughout his life, he fulfilled regular the business roles of banker and investor, but also the governmental roles of the Federal Reserve, the Securities and Exchange Commission, the Treasury, and other yet-to-be-created agencies (Samuelson, 2002, 43).

Background: Basic Economics

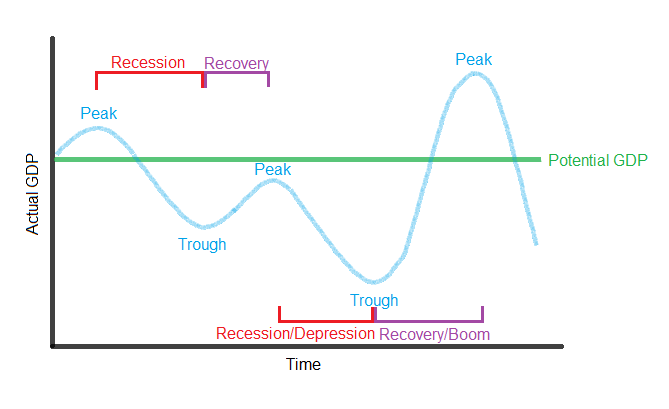

In order to really understand the impact of J.P. Morgan, one must have an understanding of some basic economic principles. First, J. P. Morgan played an influential role throughout multiple business cycles, although the premise of a "business cycle" was not defined until 1946 (Romer, 2008). The business cycle describes the natural expansion (growth) and recession (shrinkage) of the economy. Extreme expansion is a boom, while dramatic recession results in a depression. The cycle can be demonstrated by the following timeline:

As demonstrated, it is important to note that while the term "cycle" implies some regularity, there is no rule that guarantees that a recession will be followed by an expansion that will take the economy back to pre-recession levels. Additionally, nor is there any rule that dictates the length of time between a peak and a trough. Ideally, there is no need for the cycle. Once a population reaches full employment, it should be able to maintain that forever. Full employment is the ideal state when people and resources used in business and production are all used entirely, but without diminishing or wearing down the supply. In such a situation, inflation remains constant, and the effects of supply and demand remain constant (Romer, 2008).

Unfortunately, full employment is always disrupted by external influences (natural or man-made disasters, for example), and the economy therefore continues in its cycle. Less obvious forces impact the economy, too, such as technological development and population growth and movement. Of course, no recession can be explained by or blamed on one factor, and recessions are usually caused by a combination of a trigger (a tragedy, for example), ineffective policy or oversight, and natural trends.

J.P. Morgan essentially saved the United States through two recessions, the Panic of 1893 and the Panic of 1907.

Two great challenges mark those panics - the use of the gold standard, and the lack of a central bank. While the specific details of the late 1800s and early 1900s will be discussed in further depth later, one must have a firm grasp on what these challenges mean.

The gold standard was heavily debated in the latter half of the nineteenth century. The ideal behind the gold standard is that, for all of the money in circulation, there is solid gold in the United States Treasury backing it. This strengthens the U.S. dollar and minimizes inflation. Bankers, creditors, investors, and big businesses supported the gold standard because they wanted all of their money to increase in value. On the other hand, debtors, farmers and small businesses opposed the gold standard. They benefited from inflation because it granted lover interest rates and made it easier to pay off debts and loans with inflated dollars. In lieu of the gold standard, individuals formed the Greenback party, which supported paper money not backed by gold to increase circulation (Newman & Schmalbach, 2004, p.384). Others supported the unlimited coinage of silver coins to increase circulation. This idea was accomplished, to a limited extent, by the Bland-Allison Act in 1878, which demanded that the U.S. Treasury buy silver from western mines at the market price and coin between two and four million dollars per month in silver coinage at a standard silver-to-gold ratio of sixteen to one (Gordon, 2010, p.66).

In regards to a central bank, a the national Bank of the United States had been vetoed by Andrew Jackson in 1832 because he believed it to be unconstitutional. As a result, federal funds no longer supported the banks, and various state banks came into being (Newman & Schmalbach, 2004, p.190). The lack of central banks created problems, however, as "it is the business of a central bank to monitor commercial banks, regulate the money supply, and act in times of panic as the lender of last resort" (Gordon, 1989). Hence, when there is no central bank, smaller banks (state or private banks) have no lender to supply funds when their vaults are running low.

Another important theory of economics to understand in relation to J.P. Morgan's legacy is Gresham's Law.

Gresham's Law = Bad Money Drives Out Good | While Gresham's Law can be simply stated as "bad money drives out good," its actual meaning is more complex. It relates to the coinage of money. When money is coined with various metals while still holding the same legal tender, individuals will opt to hoard and even export the coinage made from the more valuable metal. This diminishes the supply of money in circulation ("Gresham's Law," 2011). This law applies to the problem faced in the Panic of 1893. |

Did you know? |  |